You’re sitting in the finance office, paperwork half-signed, when the F&I manager slides another form across the desk. “Extended warranty,” they say with that practiced smile. “Just $2,500 for complete peace of mind.”

Your brain does the math. That’s a lot of money. But what if the transmission fails? What if the engine needs work? Suddenly, you’re second-guessing everything, and that’s exactly what they’re counting on.

I’m Priya Verma, and I’ve spent five years analyzing automotive finance products and helping people navigate these exact decisions. I’ve seen the good, the bad, and the genuinely predatory warranty offers. I’ve watched people throw away thousands on coverage they never used, and I’ve also seen others dodge $8,000 repair bills because they made the right call. What I’m about to share isn’t the sanitized advice you’ll find on manufacturer websites. This is what actually happens when rubber meets road.

Here’s what nobody tells you upfront: extended warranties aren’t inherently good or bad. They’re risk management products, and whether they make sense depends entirely on your specific situation. The dealer won’t tell you this because they make 50-70% commission on these policies. That $2,500 warranty? The dealer pockets around $1,500 of it.

Let me break down exactly when these plans make financial sense, when they’re a complete waste, and how to actually calculate if you need one.

What Extended Car Warranties Actually Cover (And What They Don’t)

Extended warranties go by different names—vehicle service contracts, extended service plans, mechanical breakdown insurance—but they all do the same thing: they cover specific repairs after your factory warranty expires.

Your factory warranty typically runs 3 years/36,000 miles for bumper-to-bumper coverage and 5 years/60,000 miles for powertrain. An extended warranty picks up where that ends, usually offering coverage from 4-7 years or 75,000-150,000 miles.

Here’s where it gets messy. Not all extended warranties cover the same things.

Common Coverage Levels:

- Exclusionary (Bumper-to-Bumper): Covers everything except what’s specifically listed as excluded. This is the most comprehensive and expensive option.

- Stated Component: Covers only the parts explicitly listed in the contract. Read this list carefully—if it’s not mentioned, it’s not covered.

- Powertrain Only: Covers engine, transmission, and drive axles. Nothing else. This is the cheapest option but offers minimal protection.

I’ve reviewed hundreds of contracts, and here’s what typically gets excluded even in “comprehensive” plans:

- Wear items (brake pads, wiper blades, filters)

- Maintenance services (oil changes, tire rotations)

- Glass, body panels, and interior components

- Damage from accidents or neglect

- Modifications or aftermarket parts

- Rental car costs (unless specifically added)

That last one catches people off guard. Your car’s in the shop for two weeks waiting on a covered repair, and you’re paying $50/day out of pocket for a rental because you didn’t read the fine print.

The Real Cost Analysis: When Warranties Actually Pay Off

Let’s talk numbers, because that’s what actually matters.

The average extended warranty costs between $1,500-$4,000 depending on coverage level, vehicle, and contract length. According to Consumer Reports data, the average person files claims totaling $837 over the life of their extended warranty. That’s a net loss of $663-$3,163.

But averages lie. They hide the reality that some people never file a claim while others rack up $10,000+ in covered repairs.

Vehicle Reliability Matters More Than You Think

I analyzed repair frequency data across different brands, and the pattern is clear:

| Vehicle Brand | Avg Annual Repair Cost (Years 4-7) | Extended Warranty Break-Even Point |

|---|---|---|

| Toyota/Lexus | $350 | Rarely worth it |

| Honda/Acura | $420 | Borderline |

| Mazda | $480 | Borderline |

| Ford | $650 | Consider for complex models |

| Chevrolet | $720 | Worth evaluating |

| Ram | $850 | Often makes sense |

| Land Rover | $1,450 | Absolutely get one |

| BMW | $1,300 | Strongly consider |

If you’re buying a Toyota Camry or Honda Accord, you’re statistically unlikely to need expensive repairs during the extended warranty period. These vehicles are engineered for reliability, and their failure rates are low.

If you’re buying a German luxury vehicle or a domestic truck with advanced tech, your odds of hitting a major repair bill shoot up dramatically.

Your Driving Patterns Change The Math

Here’s where personal factors override general statistics:

- High mileage drivers (20,000+ miles/year): You’ll hit the contract’s mileage limit faster and put more wear on components. Extended warranties often make sense here.

- Short-term owners (planning to sell within 3-4 years): You probably won’t keep the car long enough to benefit. Skip it.

- Long-term owners (7+ years): You’ll likely face major repairs eventually, but many extended warranties expire before the most expensive failures occur.

- City vs highway driving: Stop-and-go traffic increases transmission wear and electrical system stress. Highway cruising is easier on vehicles.

I worked with a client who bought an extended warranty on a Subaru Outback. She drove 35,000 miles annually for work—mostly rural highways in harsh winter conditions. Her CVT transmission failed at 78,000 miles. Repair cost: $6,800. Her warranty cost: $2,200. That’s a $4,600 win.

Another client bought the same coverage on a Honda CR-V he drove 8,000 miles per year in Southern California. Zero claims in five years. He paid $1,900 for nothing.

Manufacturing Warranties vs Third-Party: The Critical Differences

Not all extended warranties come from the same place, and this matters more than most people realize.

Manufacturer Warranties (Factory-Backed)

These come directly from your vehicle’s manufacturer—Toyota, Ford, BMW, etc. They’re sold through dealerships and are honored at any franchised dealer nationwide.

Advantages:

- No questions about coverage disputes

- Dealerships don’t fight claims

- Can’t be denied because the company went bankrupt

- Usually include perks like roadside assistance and rental coverage

- Transfer to new owners (adds resale value)

Disadvantages:

- Most expensive option

- Only available on new or certified pre-owned vehicles

- Must be purchased within specific timeframes

Third-Party Warranties

These come from independent companies like Endurance, CARCHEX, or Toco Warranty. You’ll see them advertised heavily online and on TV.

Advantages:

- Available on older, high-mileage vehicles

- Often cheaper than manufacturer plans

- Can be purchased anytime

- Sometimes offer more flexible coverage options

Disadvantages:

- Claim approval rates vary wildly by company

- Some companies have terrible reputations for denying claims

- Dealerships may require authorization before repairs (delays)

- Company bankruptcy risk

- May not be accepted at all repair shops

I’ve seen third-party warranties work great, and I’ve seen them turn into nightmares. The difference is company reputation and contract specifics.

Red Flags With Third-Party Providers:

- Requiring you to use specific repair facilities

- Deductibles over $200 per visit

- “Waiting periods” before coverage begins

- Vague language about “mechanical breakdown” vs “normal wear”

- No A+ rating with the Better Business Bureau

- Mostly negative reviews focusing on claim denials

If a third-party company checks these boxes, walk away.

The Fine Print That Kills Most Extended Warranties

Contracts are written by lawyers whose job is protecting the company, not you. Here’s what actually trips people up:

Pre-Existing Conditions

Most warranties exclude anything wrong with the vehicle before the contract starts. Seems fair, right? Except many problems don’t show symptoms immediately.

Your transmission might have been slowly failing when you bought the warranty, but it didn’t fully die until three months later. The warranty company investigates, finds “evidence of pre-existing wear,” and denies your claim. You’re out the $4,200 repair AND the $2,000 warranty cost.

Maintenance Requirements

Extended warranties typically require documented proof of all scheduled maintenance. Miss one oil change? They can void your entire engine claim.

I watched someone get denied a $7,500 engine repair because they couldn’t produce a receipt for an oil change from 18 months prior. They’d done the maintenance themselves and didn’t keep records. The warranty company argued lack of proof meant lack of maintenance.

Keep every single receipt. Take photos of your odometer at each service. Store them digitally where you won’t lose them.

Betterment Clauses

Some contracts include “betterment” provisions where they only pay for the depreciated value of parts, not new replacements. Your 6-year-old alternator fails. A new one costs $600. The warranty company argues it’ll only cover $350 because that’s the depreciated value of your old part. You pay the difference.

Indirect Damage

Your water pump fails and damages your engine. The warranty covers the water pump replacement ($400) but not the engine damage ($3,500) because that’s considered “consequential damage” from the initial failure.

These clauses vary by contract, but they exist in many third-party policies specifically to limit payouts.

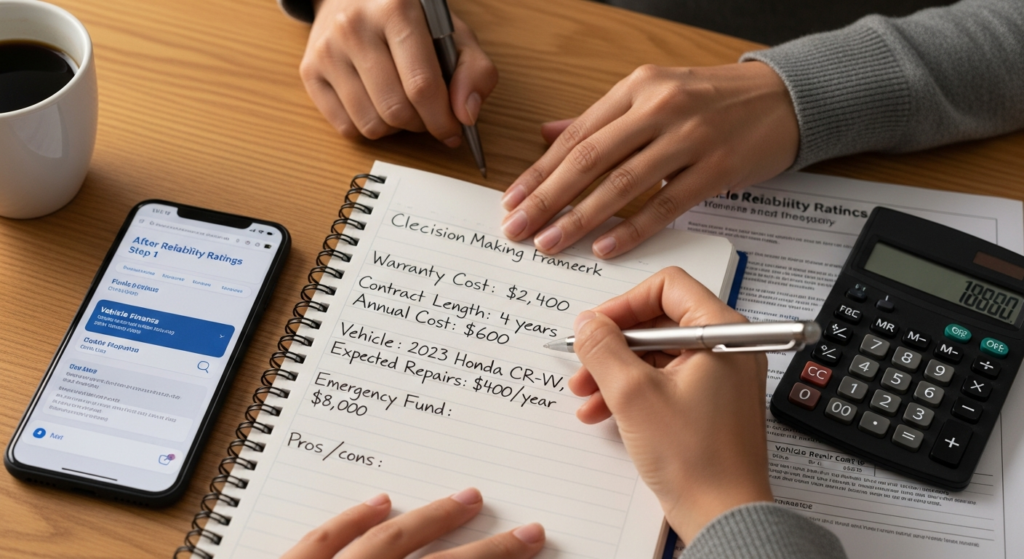

How To Actually Calculate If You Need One

Forget the emotion. Forget the sales pitch. Here’s the framework I use:

Step 1: Research Your Vehicle’s Specific Reliability

Don’t just look at brand reputation. Look up your exact model and year. A 2023 Ford F-150 with the 5.0L V8 has different reliability than the 3.5L EcoBoost. These details matter.

Resources that actually help:

- Consumer Reports reliability ratings (paid subscription, but worth it)

- NHTSA complaint database (free, shows real-world problems)

- Model-specific owner forums (search for “common problems”)

Step 2: Calculate Your Personal Risk Tolerance

Could you handle a $5,000 repair bill tomorrow without financial stress? If yes, you’re a good candidate for self-insuring (skip the warranty, save the money).

If a $2,000 unexpected expense would be financially devastating, an extended warranty functions as legitimate insurance, even if the math doesn’t perfectly favor it.

Step 3: Get Multiple Quotes

The dealer’s finance office isn’t your only option. Call your manufacturer’s customer service line. Call independent warranty companies. Get at least three quotes with identical coverage levels.

I’ve seen price variations of $1,500 for the exact same coverage just by shopping around.

Step 4: Run The Numbers

Take the warranty cost and divide it by the contract length in years. That’s your annual “insurance premium.”

Compare that to:

- Your vehicle’s expected annual repair costs (use the reliability data)

- Your emergency fund status

- Your monthly budget flexibility

If the warranty costs $2,400 for a 4-year contract, that’s $600/year or $50/month. Is that worth it to you for peace of mind? Only you can answer that.

When To Buy And When To Walk Away

Buy an extended warranty if:

- You’re purchasing a luxury European vehicle (German, British, Italian)

- You’re buying a domestic truck or SUV with complex tech (adaptive cruise, cylinder deactivation, etc.)

- You drive significantly above average mileage

- You plan to keep the vehicle 7+ years

- You have limited savings for emergency repairs

- The vehicle has a known expensive failure point (research this!)

Skip the extended warranty if:

- You’re buying a Toyota, Honda, or Mazda with good reliability ratings

- You have a solid emergency fund (6+ months expenses)

- You’re planning to sell within 3-4 years

- The warranty costs more than 5% of the vehicle’s purchase price

- You’re buying a used vehicle with over 100,000 miles (many won’t cover it anyway)

The Middle Ground: Consider It If:

- You’re buying American or Korean brands (mixed reliability)

- You drive average mileage (12,000-15,000/year)

- You can negotiate the price down 30-40% from the initial offer (yes, this is possible)

Negotiating Extended Warranty Prices (They Expect You To)

Here’s something the finance manager won’t tell you: those prices aren’t fixed. Everything in the finance office is negotiable, including extended warranties.

The dealer’s cost on that $3,000 warranty might be $1,200. They’re marked up significantly because most people don’t negotiate.

Tactics that actually work:

Tell them you’re not interested and stand up to leave. This isn’t a bluff—mean it. The price will suddenly drop $500-800.

Get quotes from online warranty providers and show them. “CARCHEX is offering similar coverage for $1,800. Can you match that?”

Buy the warranty later. You usually have until your factory warranty expires to purchase an extended plan directly from the manufacturer at significantly lower prices than the dealership offers.

Ask about cancellation terms upfront. Many warranties are cancelable for a prorated refund. If you sell the vehicle early, you get money back.

I’ve negotiated extended warranties from $2,800 down to $1,650 just by being willing to walk away and showing competing quotes.

The Alternative: Self-Insuring With A Vehicle Repair Fund

Here’s the strategy nobody in the automotive industry wants you to consider: save the warranty money yourself.

Take that $2,500 you’d spend on an extended warranty and put it in a high-yield savings account. Don’t touch it except for vehicle repairs.

Why this often makes more sense:

- If you don’t need repairs, you keep the money

- The money earns interest instead of going to a warranty company

- No claims to file, no authorizations needed, no deductibles

- You can use it for any repair, not just “covered” components

- It’s available for any vehicle you own, not just one

The catch: this requires discipline. You can’t raid the fund for vacation or shopping. It’s insurance you provide for yourself.

Over five years with a reliable vehicle, you might spend $2,000 on repairs while having $2,500+ sitting in the account. That’s better than buying a warranty you never use.

What Happens When Claims Get Denied

Let’s talk about the worst-case scenario because it happens more often than warranty companies admit.

Your transmission fails. You file a claim. The warranty company sends an inspector who finds “evidence of abuse” or “lack of maintenance” or claims it’s “normal wear and tear.” Claim denied.

Now what?

Your escalation options:

- Request a detailed written explanation of the denial

- Gather all maintenance records and appeal in writing

- Get an independent mechanic’s opinion contradicting their finding

- File a complaint with your state’s insurance commissioner

- Consider small claims court if the amount is under your state’s limit ($5,000-10,000 typically)

I helped a colleague fight a denied claim on his Jeep’s transfer case. The warranty company claimed “off-road abuse.” He’d never taken it off pavement. He appealed with photos showing pristine undercarriage, all service records, and a mechanic’s statement that the failure was manufacturing defect, not abuse. They reversed the denial after three weeks of back-and-forth.

Most people give up after the first denial. The warranty companies count on this.

How Extended Warranties Affect Vehicle Resale Value

Here’s an underrated benefit of manufacturer-backed extended warranties: they transfer to the next owner.

If you’re selling a used vehicle with two years of bumper-to-bumper coverage remaining, that’s a legitimate selling point. Buyers pay more for vehicles with warranty coverage remaining.

I’ve seen used car prices increase $800-1,500 when transferable warranty coverage is included. This doesn’t fully offset the warranty cost, but it reduces your net expense.

Third-party warranties rarely transfer, or they charge $50-75 fees to do so, which makes them less valuable for resale.

Specific Vehicle Types And Warranty Recommendations

Electric Vehicles

EVs have fewer moving parts than gas vehicles, which sounds like you don’t need a warranty. Wrong. The battery and electric motor systems are expensive if they fail, and many aren’t covered by extended factory warranties.

If you’re buying a Tesla, Rivian, or any EV from a newer manufacturer, strongly consider extended coverage. These companies are still working out reliability issues.

Established manufacturers like Chevrolet (Bolt) or Ford (Mustang Mach-E) typically offer good factory warranties. Still, verify what happens if the battery degrades below 70% capacity during your ownership.

Pickup Trucks

Modern trucks are complex. They have cylinder deactivation systems, advanced 10-speed transmissions, adaptive cruise control, and towing packages that put enormous stress on components.

Ram trucks, in particular, have higher-than-average electrical system failures and transmission issues. An extended warranty on a Ram 1500 often pays for itself.

Ford F-150s with the EcoBoost engines have turbocharger issues in higher mileage. If you’re buying one, factor this into your warranty decision.

Used Luxury Vehicles

This is where extended warranties shine. A used BMW 5-Series might only cost $25,000, but repairs still cost BMW prices. A single air suspension failure runs $3,000-4,000.

If you’re buying used luxury, budget for either a warranty or significantly higher repair reserves.

Frequently Asked Questions

Can I buy an extended warranty after my factory coverage expires?

Sometimes, but your options are limited to third-party providers, and they’ll often require a vehicle inspection before approval. Pre-existing conditions won’t be covered. Your best move is buying before your factory warranty ends.

What if I pay off my car loan early—can I cancel the warranty?

Most warranties purchased through dealers are cancelable for a prorated refund within the first 30-60 days at full refund, then prorated based on time and mileage used. If you financed the warranty with your car loan, the refund goes to the lienholder to reduce your principal balance.

Do extended warranties cover rental cars while mine is being repaired?

Some do, most don’t unless you specifically pay extra for rental coverage. Always check this before buying. Daily rental costs add up fast if you’re waiting on parts for two weeks.

Are “bumper-to-bumper” warranties really comprehensive?

No. Even the most comprehensive plans exclude wear items, maintenance, and specific components. Read the actual exclusions list in your contract. “Bumper-to-bumper” is marketing language, not a literal guarantee.

The Bottom Line: Making Your Decision

Extended warranties aren’t scams, but they’re not必要的 either. They’re risk management products with built-in profit margins.

The financially optimal decision for most people buying reliable vehicles is to skip the warranty and self-insure. But optimal isn’t always practical. If you can’t afford a surprise $4,000 repair bill and you’re buying a vehicle with questionable reliability, the warranty provides legitimate value even if the math doesn’t perfectly support it.

What I absolutely don’t recommend: buying an extended warranty in the finance office without research because you’re tired and just want to finish signing papers. That’s when you make expensive mistakes.

Take the contract home. Read it completely. Compare prices. Sleep on it. You usually have 30 days to add coverage after purchase—use that time wisely.

The best extended warranty is the one you never need to use because you bought a reliable vehicle in the first place. But if you’re worried about repair costs, and you’ve done the research, and the numbers make sense for your situation, there’s nothing wrong with buying peace of mind.

Just make sure you’re buying actual coverage, not just expensive paperwork that’ll fight you when you need it most.